While entrepreneurs can learn from Mustafa Centre's success, the average Singaporean can draw money lessons from it too.

First published on 7 October 2016. Last updated on 12 January 2017.

Mustafa Centre is Singapore’s biggest 24 hour retail mall. It’s also one of the biggest unofficial tourist attractions in the country, bringing in everyone from budget travellers to high-end hotel dwellers.

But while many have pondered the business lessons of Mustafa Centre, there are personal finance lessons Singaporeans can draw from it too.

The History of Mustafa Centre

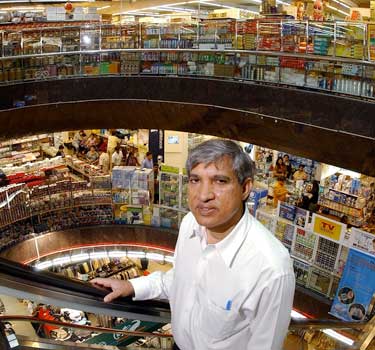

Mustafa Centre is a 24 hour retail mall along Syed Alwi Road, in Little India. The current managing director and co-founder of Mustafa Centre, Mustaq Ahmad, was initially a small business owner.

Mustaq Ahmad was born in Uttar Prasdesh, India, on 8th June 1951. He joined his father in Singapore in 1956, when the two ran a pushcart selling tea and bread. Over time, Mustaq saved sufficient capital to start his own business selling handkerchiefs, next to his father’s stall.

This grew to a fabric and textiles business, in which his father eventually joined him. At Secondary Four, Mustaq dropped out of school to run the business full-time with his father.

Following a ban on street stalls in the 1970s, Mustaq and his father opened a proper, ready-made clothing store along Campbell Lane. This was a bold move; at the time, it was more common for people to buy fabrics and sew the clothes at home, than to purchase it off the rack.

The store was named after Mustaq’s father and uncle, and the company that owns Mustafa Centre continues to bear the name: Mohamed Mustafa & Samsuddin.

The business eventually expanded to include another outlet at Serangoon Road, which became the main retail outlet (the original store was relegated to a sort of warehouse). Mustaq expanded the product range to include electronics, and did something completely crazy for the time: he fixed the prices on everything. This seems normal to us now, but at the time, it was expected that you would bargain with the shop owner for everything.

At any rate, this stroke of genius grew the business and customer traffic significantly. By 1985, when the government re-acquired the shophouse store, Mustaq could move into a major retail mall. This was Serangoon Plaza, formerly known as President Shopping Centre.

When Serangoon Plaza’s management apparently lost their minds and decided to raise rent by 70 per cent, Mustaq left and bought 20 shophouses along Syed Alwi Road. These were developed into a 75,000 square foot retail mall, which opened in 1995. By 2003, the retail mall was open 24 hours, had won a tourism award (despite never deliberately attempting to win one), and brings in an estimated $302 million per year.

In 2008, Mustaq Ahmad made it to the Forbes list of the 40 richest Singaporeans (at number 38), and his business continues to expand.

What Personal Finance Lessons Can Singaporeans Learn From Mustafa?

In terms of business, whole books can be written about Mustafa Centre. But there are a lot of personal money lessons Singaporeans can learn from this as well.

1. Always Diversify

Mustafa Centre sells a massive range of products, from jewellery to electronics. This diversity isn’t just good for consumers, it provides protection from market fluctuations.

For example, when gold prices are unfavourable, the jewellery business may suffer. But unrelated businesses, such as groceries and electronics, can make up for its weaker performance. In order for the entire mall’s business to do poorly, all the assorted businesses have to be underperforming (a rare economic situation).

Now in terms of business, this is a controversial approach. Some business schools advice focusing on top selling products, and dropping the others. But in terms of personal finance, it’s a good rule to follow.

Instead of investing in just one thing, such as only mutual funds or only gold, aim for a balanced mix of assets. This will ensure that, if one of your assets falls in value, it can be compensated for by another.

A qualified wealth manager can help you to build a well-diversified portfolio of assets.

2. Be Hands-On with Your Assets

Mustaq Ahmad was - and still is - famous for the way he “walks the floor”. Most of the staff at Mustafa can attest to seeing him be the first to arrive and the last to leave. This hands-on approach to his business ensures he is aware of various threats and opportunities, and can respond fast.

Most of us dream of purely passive income. That is, an income source which delivers with no effort on our part. In reality, this is only partially possible. Even if you have passive income sources, such as indexed funds or property to rent, you must still make an effort to check on them.

You do have to ensure your fund performs as advertised, or that your property asset is not losing value due to wear and tear. There is an old saying that “what gets measured gets managed”. If you can’t tell what’s in your funds off the top of your head, or don’t know its performance last quarter, you are not measuring it.

3. The Conventional Way Isn’t Always the Best Way

Mustaq Ahmad took a bold move when he used fixed prices for everything. This was not the usual way to sell at the time. However, fixing prices solved a huge number of inefficiencies.

Fixed prices make financial planning easier, as cash flow is inconsistent if goods can be sold at different prices. It also makes it possible to service more customers, at a faster pace. Imagine if today, everyone bargained grocery prices at the supermarket checkout.

Just because everyone is doing something, that doesn’t mean it’s the best approach. Never buy an asset just because everyone else is buying it, or use a particular bank just because it’s the most common one. Think carefully about your financial needs, and do what serves you best.

4. Take Measured Risks

Mustafa Centre wouldn’t be what it is if no risks were taken in its history. Moving to Serangoon Plaza, away from the shopping heart of Little India (in the past it was a busy as Orchard Road today), was a big risk.

Fixing prices and selling ready-made clothes, along with building a mall instead of renting or buying spaces, were all risks.

However, the risks taken by Mustafa Centre have always been measured. In the early 2000’s, for example, Mustafa Centre also sold used cars. When the business didn’t do well, they pulled the plug without serious damage. There was a contingency plan for failure.

You can use the same approach. For example, you could make it a point to save up six months of your income before attempting to switch jobs. You could have a plan to restructure your debt, should your education cost more than you expect.

In short, you need to take risks to grow your income and find new opportunities. But always have a fallback plan, and do not take a risk if the consequences of failure are too high.

5. Small Savings Can Build a Large Fortune

Mustafa Centre is known for having some of the lowest prices. They can afford to do this and still stay profitable, because of detailed attention to their supply chain. They minimise the number of middlemen they have to work with (sometimes cutting them out altogether), and pay close attention to seasonal product cycles to avoid overstocking.

Hundreds, perhaps thousands of small details are addressed. This saves a little bit of money, but the cumulative effect is significant.

You can apply the same principles to your own finances. You may think that saving an extra S$20 a week is immaterial, for example. But if you put aside S$20 a week at age 30, and put the saved monthly amount in a fund that grows at five per cent per annum, you will have around S$80,475 at retirement.

That could be sufficient to clear out the last of your debts, or pay for a vacation to Europe once a year, for the next 13 years (assuming S$6,000 per trip).

One simple way to save S$20 a week is to use a cashback credit card liike the OCBC 365 Card as a mode of payment. Pay through the card to receive a rebate, and then repay the card in full to avoid paying interest. You can find the best cashback deals on SingSaver.com.sg.

Read This Next:

Similar articles

Want to Be Rich? Acting Like a Psychopath Might Help

The 11 Best Indian Restaurants In Singapore

5 Insights From Warren Buffett’s Letter For Your Investing To-Do List

A Guide To Bankruptcy In Singapore (And 3 Lessons To Learn)

Deepavali Shopping Guide 2020

Money Lessons We’ve Learnt While Binge Watching Korean Dramas

9 Life-Changing Money Lessons Singaporeans Can Learn from Star Wars

9 Money Lessons New Graduates in Singapore Should Learn

Back to Blog

Back to Blog