FII experience investing in Indian equities and some learnings for domestic households

FII experience investing in Indian equities and some learnings for domestic households

Post the economic liberalisation in 90s and opening up of capital markets, Foreign Investors over time have backed many an Indian entrepreneur, in the process owning valuable stakes in many well-run Indian companies – even as Indian households continued to traditionally back physical assets of real estate and gold. It has only been in recent years that Indian households have meaningfully started to allocate to Indian equities, as a proportion of their savings.

It would be worthwhile to see the experience of foreign investors as a collective and try and glean some learnings for Indian households that can help condition behaviour in the decades ahead.

Firstly, let us see what foreigners have brought into Indian equities and how much is it worth?

From the turn of this millennium to 30 June 2022, FII have deployed net US$165bn buying Indian equities, and value of stake as of 30 June 2022 (in BSE500 companies) is US$537bn. There have been 5608 trading days from 1 Jan 2001 to 30 June 2022 overall, FPI have net purchased 408bn$ on 64% of these days, while they have net sold on 36% of days, cumulatively selling 243bn$. (Thus, net deployment of 408bn-243bn = 165bn$). The peak value of FII stake was US$672bn as of Sep 2021, total net deployment from Jan 2001 till Sep 2021 was about 198bn$.

FII are therefore sitting on profits (difference of their stake as on 30 June 2022 and their total deployment since 2001) of 372bn$ (down from peak profits of 474bn$, result of FII selling in last 12 months, some fall in the companies they held stakes in and depreciation of rupee). These are staggering sums in absolute terms – backing good companies and letting time do their magic of compounding.

Given we have their collective activity on any given trading day, it is easy to compute their IRR of their investments. Analysis of data from 2005 till 2022 – reveals that IRR have broadly been in 8-11% range in the last decade. These IRR are in dollar terms and during this period from June 2005 to June 2022, INR has depreciated by 3.56% on an annualised basis. IRR of 8-11% in dollar terms need to be also evaluated in context of relatively lower cost of capital seen during most of last decade, as well as sub-par returns made in most other markets and asset classes (barring US). Allocators to Indian equities have been well rewarded.

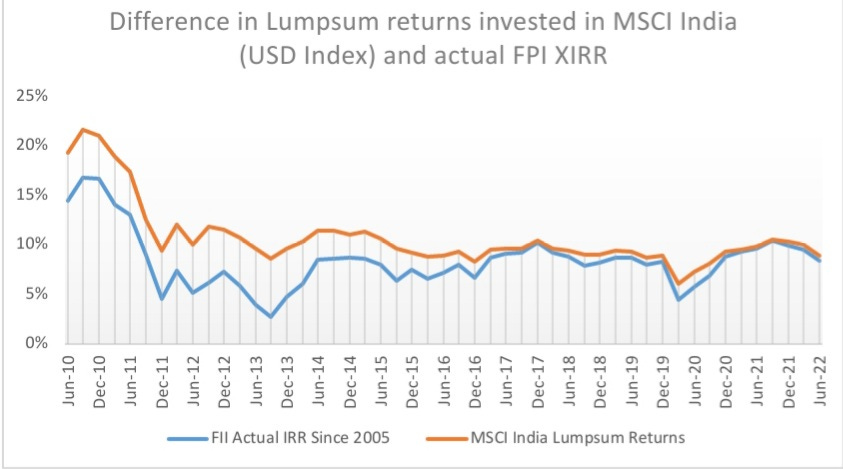

While, FII overall allocation to Indian equities have seen broadly satisfactory outcome, if one sees their purchase pattern, one sees a clear pro-cyclical tilt. Whenever Indian markets correct, and there has been a significant rise in volatility, FII have sold Indian equities and have come back after the dust settles.

Volatility is not a bug, but a feature of asset classes like equities. And while it is tempting that one can sit out during periods of turbulence and to get back in one dust settles in, it exacts a reasonably high price. As shown below, FII IRR have been lower than lumpsum investing return in MSCI India index, over most parts of last decade.

So what lessons can domestic households who have recently started allocating to equities take from FII experience?

Think long term – Investment is a marathon, there are many goals which are long-term, allocating to Indian equities to plan for such goals

Ofcourse, compounding works only if one invests in sound companies, which have a track-record and ability to re-invest profits in their businesses and generate returns ahead of their cost of capital

Volatility is not a bug, but a feature of asset classes – SIP experience we have seen so far demonstrates the maturity of Indian household – to overlook transient phases of volatility. Please keep at it, especially for your longer-term goals. Of course, it doesn’t mean to mindlessly buy every dip, but have a sound financial plan – basis valuations, opportunity cost in other asset classes – keep a plan ready for asset allocation.

Make the allocation count – most households still have significant allocation to physical assets (gold, real estate). Asset allocation is predominant driver of overall household wealth formation.

Lastly, keep return expectations realistic! Last few years post pandemic has seen return expectation amongst investors move up significantly, it may be worthwhile to remember FII experience across decades of high single digit dollar returns. There were times, when IRR did drop to 3-4% as well, but those phases didn’t last very long, and in hindsight were great opportunities for long-term allocators of capital.

(Version of this published at :

https://www.moneycontrol.com/news/opinion/fii-experience-in-india-holds-key-lessons-for-retail-investors-9274971.html)